Koh Samui has emerged as one of Southeast Asia’s most attractive destinations for American property investors and retirees seeking tropical paradise combined with solid investment returns. With its pristine beaches, world-class infrastructure, and welcoming expat community, the island offers an appealing alternative to increasingly expensive US coastal markets.

However, for US citizens, buying property in Thailand presents unique challenges that go far beyond the standard foreign ownership restrictions. Unlike investors from other countries, Americans must navigate a complex dual-jurisdiction landscape that includes not only Thai property law but also extensive US tax reporting requirements under FBAR and FATCA regulations.

This comprehensive guide addresses the specific concerns of US citizens considering Koh Samui property investment. We’ll cover everything from ownership structures and legal processes to US tax obligations and currency strategies, providing you with the complete roadmap you need to make informed decisions while remaining compliant with both Thai and American regulations.

Can US Citizens Buy Property in Thailand?

Yes, US citizens can buy property in Thailand, but with significant restrictions.

Thailand’s Land Code Act of 1954 prohibits foreigners from owning land freehold. However, several legal pathways exist for US citizens to secure property interests:

What US Citizens CAN Buy:

Freehold Condominiums

- Foreigners can own condominium units outright (freehold) in their personal name

- Limited to 49% of the building’s total sellable area

- Must comply with foreign exchange transaction requirements (FET Form)

- The most straightforward option for US investors

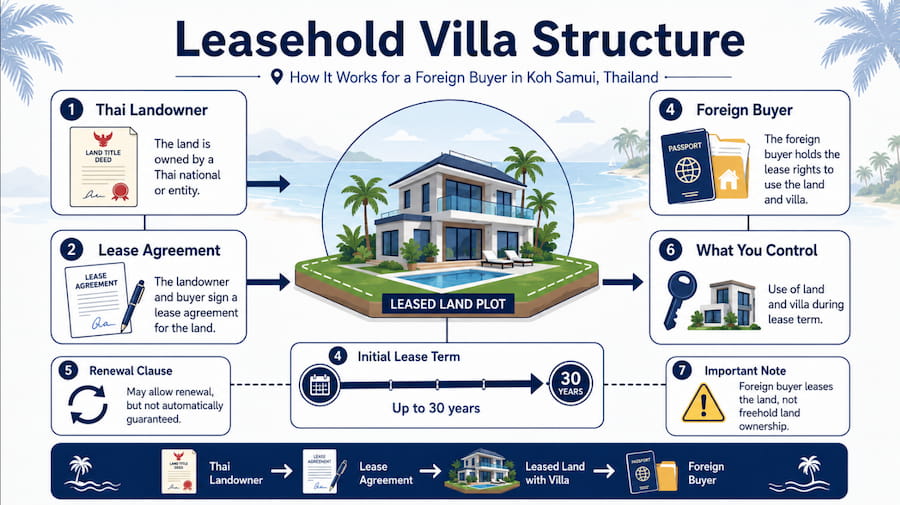

Leasehold Agreements

- Foreigners can lease land for up to 30 years (initial term)

- Renewable for additional 30-year periods (though renewal isn’t legally guaranteed)

- Common structure for villa purchases on leased land

- Can include purchase option clauses in some cases

Through a Thai Limited Company

- Foreigners can own up to 49% of a Thai company that owns land

- Complex structure requiring Thai majority shareholders

- Must demonstrate legitimate business activity

- Increased regulatory scrutiny in recent years

What US Citizens CANNOT Buy:

- Agricultural land (strictly prohibited)

- Land freehold in personal name

- More than 49% of any condominium building’s foreign quota

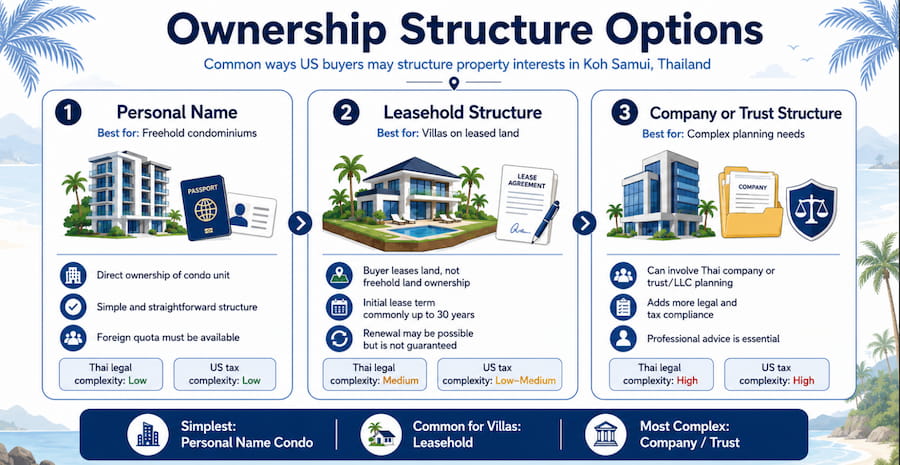

What Are The Ownership Structure Options?

Choosing the right ownership structure isn’t just about Thai law, it’s about optimising your US tax position. Here’s how each option affects your American tax obligations:

Option 1: Personal Name Ownership (Condominium Only)

Thai Law: Simplest structure. You own the condo freehold in your name.

US Tax Implications:

- Property held personally is straightforward for US tax purposes

- Rental income reported on Schedule E

- Depreciation available (residential: 27.5 years)

- Capital gains taxed at favourable long-term rates if held >1 year

- Must file FBAR if foreign financial accounts exceed $10,000 aggregate

- FATCA reporting required if foreign assets exceed thresholds ($200,000 single, $400,000 married filing jointly)

Best For: Single-property investors, those seeking simplicity, retirees planning personal use

Option 2: Thai Limited Company

Thai Law: Company owns the land/property; you own up to 49% of the company.

US Tax Implications:

- CRITICAL: Thai companies are typically classified as Controlled Foreign Corporations (CFCs) for US tax purposes

- Subpart F income rules may apply to rental income

- Complex Form 5471 filing requirements (Information Return of US Persons With Respect to Certain Foreign Corporations)

- Potential for double taxation without careful planning

- Professional tax advice absolutely essential

Best For: Commercial investments, multiple properties, those with existing business structures

Option 3: US LLC or Trust Ownership

Thai Law: The LLC/trust cannot directly own land, but can own condominium units or be the beneficiary of leasehold structures.

US Tax Implications:

- Maintains US tax efficiency and estate planning benefits

- Disregarded entity LLCs offer pass-through taxation

- Trust structures provide asset protection and succession planning

- Can complicate Thai legal processes

Best For: Estate planning concerns, asset protection priorities, sophisticated investors

Comparison Matrix

| Factor | Personal Name | Thai Company | US LLC / Trust |

| Thai Legal Complexity | Low | High | Medium |

| US Tax Complexity | Low | Very High | Medium |

| Estate Planning | Limited | Complex | Excellent |

| Asset Protection | Limited | Moderate | Good |

| FBAR Required | Yes | Yes | Yes |

| FATCA Reporting | Yes | Yes | Yes |

| Annual Compliance Cost | Low | $2,000–$5,000 | $500–$2,000 |

How Does Buying Process for Americans Look Like?

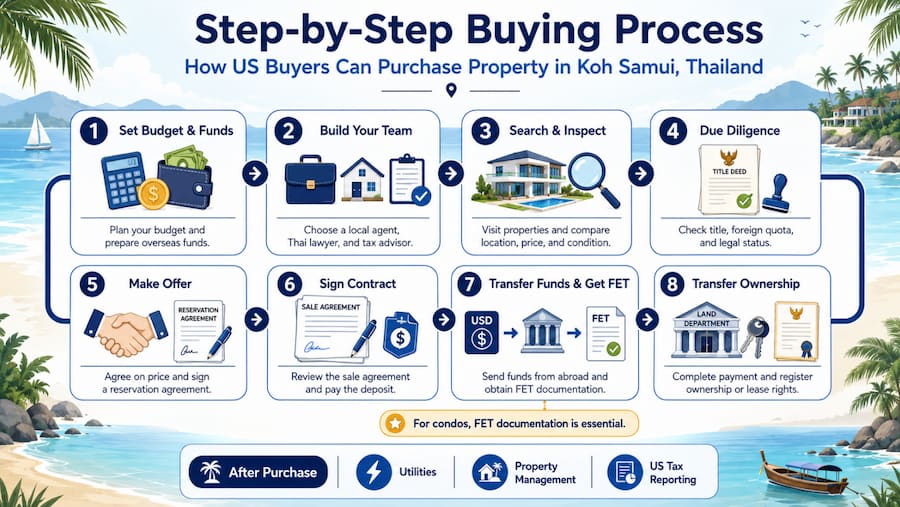

Phase 1: Pre-Purchase Preparation (Weeks 1-4)

- Secure Financing or Funds

- Thai banks rarely lend to foreigners; expect cash purchases

- If financing, explore Singapore or Hong Kong banks

- Prepare funds for international transfer

- Open Thai Bank Account

- Required for foreign exchange transaction (FET) documentation

- Bring passport, proof of address, and reference letter

- Kasikorn Bank, Bangkok Bank, and SCB are foreigner-friendly

- Engage Professional Team

- Real Estate Agent: Local expertise, property sourcing

- Thai Lawyer: Contract review, due diligence, transfer supervision

- US Tax Advisor: FBAR/FATCA compliance, structure optimization

- Define Search Criteria

- Budget in USD (account for exchange rate fluctuations)

- Preferred areas (Chaweng, Bophut, Lamai, Maenam)

- Property type (condo vs. villa)

- Investment vs. personal use priorities

Phase 2: Property Search and Offer (Weeks 5-8)

- Property Viewing

- Visit Koh Samui for in-person inspection (highly recommended)

- Evaluate: location, condition, building management, surrounding development

- Verify foreign quota availability for condos

- Initial Due Diligence

- Title deed (Chanote) verification

- Check for encumbrances or liens

- Confirm seller ownership and authority to sell

- Review building regulations (for condos)

- Make Offer

- Negotiate price (typically 5-15% below asking)

- Sign reservation agreement (usually 50,000-100,000 THB)

- Include due diligence contingency period

Phase 3: Contract and Closing (Weeks 9-12)

- Sales Agreement Execution

- 10% deposit typically required upon contract signing

- Clearly specify payment schedule and transfer date

- Include penalty clauses for breach

- Foreign Exchange Transaction (FET Form)

- CRITICAL for condo purchases: Funds must be transferred from abroad in foreign currency

- Bank converts to THB and issues Foreign Exchange Transaction Form (FET)

- FET proves funds came from overseas and is required for foreign ownership registration

- Keep all documentation for future resale

- Final Due Diligence

- Comprehensive title search

- Verification of no outstanding taxes or utility bills

- Building inspection (structural, electrical, plumbing)

- Review of condominium regulations (if applicable)

- Transfer at Land Department

- Both parties present at local Land Department office

- Balance of payment made

- Transfer taxes and fees paid

- New title deed (Chanote) issued in buyer’s name

Phase 4: Post-Purchase (Ongoing)

- Utility Transfers

- Electricity (PEA) and water (Provincial Waterworks)

- Internet and cable services

- Property Management Setup

- Essential for rental properties

- Services typically include: tenant management, maintenance, cleaning, bill payment

- Fees: 15-20% of rental income

- US Tax Compliance Setup

- File FBAR (FinCEN Form 114) if applicable

- Report foreign assets on Form 8938 (FATCA) if thresholds met

- Establish system for tracking rental income and expenses

Thai Taxes and Fees: Complete Breakdown

Understanding the total cost of ownership is essential for accurate ROI calculations. Here’s what to budget:

One-Time Purchase Costs

| Fee | Rate | Typical Cost (USD) |

| Transfer Fee | 2% of appraised value | $4,000–$20,000 |

| Stamp Duty | 0.5% if owned for more than 5 years | $1,000–$5,000 |

| Specific Business Tax | 3.3% if owned for less than 5 years | $6,600–$33,000 |

| Withholding Tax | Progressive rate, usually 1%–35% | Varies |

| Legal Fees | Fixed fee or percentage-based | $1,500–$5,000 |

Note: Transfer fees are typically split 50/50 between buyer and seller, but this is negotiable.

Annual Ownership Costs

| Expense | Typical Annual Cost (USD) |

| Property Tax | 0.02%–0.1% of appraised value |

| Common Area Fees (Condos) | $1,000–$3,000 |

| Property Management | 15%–20% of rental income |

| Insurance | Around 0.1% of property value |

| Maintenance Reserve | 1%–2% of property value |

What US Tax Obligations Should Buyers Know Before Purchasing Property in Thailand?

This is where US citizens face requirements that other foreign buyers don’t. Failure to comply can result in severe penalties.

FBAR (FinCEN Form 114)

What It Is: Report of Foreign Bank and Financial Accounts

Who Must File: Any US person with aggregate foreign financial accounts exceeding $10,000 at any point during the calendar year

What Counts:

- Thai bank accounts

- Foreign securities accounts

- Foreign mutual funds

- Foreign life insurance with cash value

Deadline: April 15 (automatic extension to October 15)

Penalties for Non-Compliance:

- Non-willful violations: Up to $10,000 per violation

- Willful violations: Greater of $100,000 or 50% of account balance

- Criminal penalties possible for willful non-filing

How to File: Electronically through BSA E-Filing System

FATCA (Form 8938)

What It Is: Statement of Specified Foreign Financial Assets

Who Must File:

- Single taxpayers: Foreign assets exceeding $200,000 on last day of year OR $300,000 at any time

- Married filing jointly: $400,000 on last day OR $600,000 at any time

- Lower thresholds apply if living abroad

What to Report:

- Foreign bank accounts (also reported on FBAR)

- Foreign stock/securities

- Foreign partnership interests

- Foreign-issued life insurance

- Foreign annuity contracts

- Foreign real estate held through foreign entity

Deadline: With your annual tax return (April 15)

Penalties:

- $10,000 for failure to disclose

- Additional $10,000 for each 30 days of continued failure (after IRS notice)

- Maximum penalty: $50,000

- Criminal penalties possible

Rental Income Reporting

Taxable Income: Gross rental income minus allowable expenses

Allowable Expenses:

- Property management fees

- Repairs and maintenance

- Insurance

- Property taxes

- Depreciation (27.5 years for residential)

- Travel expenses (if primarily for property management)

- Legal and professional fees

Reporting: Schedule E (Supplemental Income and Loss)

Foreign Tax Credit: Taxes paid to Thailand can offset US tax liability

Capital Gains Tax

US Tax Treatment:

- Held >1 year: Long-term capital gains rates (0%, 15%, or 20% depending on income)

- Held <1 year: Ordinary income rates

Thai Tax Treatment:

- Withholding tax applies at transfer (progressive rates 1-35%)

- Can credit Thai withholding against US liability

Currency Considerations:

- Gain/loss calculated in USD

- Exchange rate at purchase vs. sale affects taxable gain

- Can result in US taxable gain even if THB-denominated value decreased

Estate Tax Implications

US Estate Tax:

- Applies to worldwide assets for US citizens

- 2026 exemption: $13.99 million per individual

- Property in Thai company may have different treatment

- Proper structuring essential for high-net-worth individuals

Thai Estate Tax:

- Thailand has no estate tax

- Inheritance process can be complex and time-consuming

- Will should be drafted under Thai law

How Should US Buyers Plan Their Currency Exchange Strategy from USD to THB?

For American investors, currency fluctuations can significantly impact returns. A 10% swing in the USD/THB exchange rate can mean the difference between profit and loss.

Historical Context

- Current Rate (2026): Approximately 34-35 THB per USD

- 5-Year Range: 30-37 THB per USD

- 10-Year Average: Approximately 33 THB per USD

Timing Strategies

- Dollar-Cost Averaging

- Transfer funds in tranches rather than lump sum

- Reduces impact of unfavorable single-day rates

- Particularly useful for large purchases

- Forward Contracts

- Lock in exchange rate for future transfers

- Available through major banks and forex brokers

- Requires deposit and commitment to future transfer

- Limit Orders

- Set target exchange rate for automatic execution

- Useful when you have flexibility on timing

- Monitor rates through XE, Wise, or banking apps

Transfer Methods

| Method | Speed | Cost | Best For |

| Bank Wire | 3–5 days | $25–$50 plus exchange-rate spread | Large transfers and FET documentation |

| Wise / TransferWise | 1–2 days | Low fees with mid-market exchange rate | Smaller transfers and speed priority |

| OFX / TorFX | 2–4 days | Negotiated rates for larger amounts | Transfers above $50,000 |

| Cryptocurrency | A few hours | Variable fees and exchange-rate risk | Experienced users only |

Critical for FET: Funds must arrive in Thailand in foreign currency (USD) and be converted by the receiving Thai bank. Pre-converted THB transfers won’t qualify for foreign ownership documentation.

What Should Be Included in a Due Diligence Checklist for US Buyers?

Legal Verification

- [ ] Title deed (Chanote) authenticity verified at Land Department

- [ ] No encumbrances, mortgages, or liens on property

- [ ] Seller has legal authority to sell (power of attorney if applicable)

- [ ] Foreign quota availability confirmed (condominiums)

- [ ] Building permits and licenses verified (villas)

- [ ] Environmental clearances obtained (coastal properties)

Financial Verification

- [ ] All property taxes current

- [ ] No outstanding utility bills

- [ ] Common area fees paid current (condominiums)

- [ ] Seller’s withholding tax calculation reviewed

- [ ] Total closing costs estimated and budgeted

Physical Inspection

- [ ] Structural integrity assessed by professional

- [ ] Electrical systems inspected

- [ ] Plumbing and water systems tested

- [ ] Air conditioning units serviced and operational

- [ ] Roof condition evaluated

- [ ] Pest inspection completed

Documentation

- [ ] Sales agreement reviewed by independent Thai lawyer

- [ ] FET Form requirements explained and planned

- [ ] Condominium regulations reviewed (if applicable)

- [ ] Property management agreement template reviewed

US Tax Preparation

- [ ] FBAR requirements understood

- [ ] FATCA thresholds calculated

- [ ] Ownership structure optimized for US tax

- [ ] US tax advisor engaged

- [ ] System for tracking rental income/expenses established

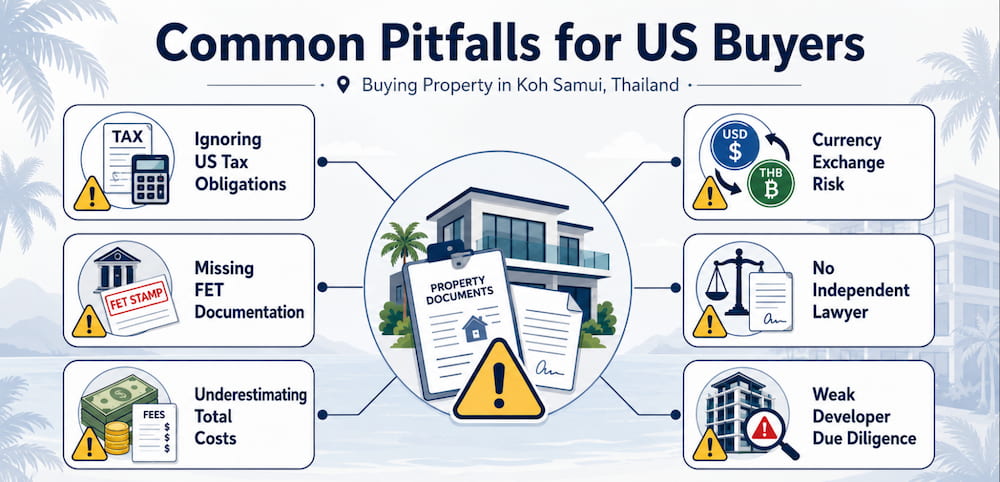

Common Pitfalls for US Buyers

1. Ignoring US Tax Obligations

The Mistake: Focusing only on Thai legal compliance while neglecting FBAR, FATCA, and rental income reporting.

The Cost: Penalties ranging from $10,000 to 50% of account balances, plus potential criminal liability.

The Solution: Engage a US tax advisor with international experience BEFORE closing.

2. Failing to Obtain FET Documentation

The Mistake: Transferring funds already converted to THB or using informal transfer methods.

The Cost: Inability to register foreign ownership, potential loss of reservation deposit.

The Solution: Work with Thai bank to ensure proper foreign exchange transaction documentation.

3. Underestimating Total Cost of Ownership

The Mistake: Budgeting only for purchase price without accounting for taxes, fees, and ongoing costs.

The Cost: Cash flow problems, forced distress sale.

The Solution: Budget 5-8% of purchase price for closing costs, plus 2-3% annually for ownership costs.

4. Overlooking Currency Risk

The Mistake: Ignoring USD/THB exchange rate impact on investment returns.

The Cost: Significant reduction in ROI or actual losses when converting back to USD.

The Solution: Develop currency strategy, consider timing of repatriation, hedge large exposures.

5. DIY Legal Approach

The Mistake: Using seller’s lawyer or skipping independent legal representation.

The Cost: Undisclosed encumbrances, defective title, unfavorable contract terms.

The Solution: Always engage independent Thai lawyer representing YOUR interests.

6. Inadequate Due Diligence on Developers

The Mistake: Buying off-plan or from developers without verifying track record.

The Cost: Project delays, quality issues, developer bankruptcy.

The Solution: Research developer history, visit completed projects, verify financial stability.

Conclusion: Your Path to Koh Samui Property Ownership

Buying property in Koh Samui as a US citizen requires navigating two complex regulatory systems simultaneously. While the process involves more paperwork and planning than domestic real estate investment, thousands of Americans have successfully built portfolios and retirement homes on the island.

The keys to success are:

- Assemble the right team; Thai lawyer, US tax advisor, and experienced real estate agent

- Understand total costs; including both Thai fees and US tax compliance

- Plan for currency exposure; develop a USD/THB strategy

- Stay compliant; FBAR and FATCA are not optional

- Choose the right structure; personal ownership works for most individual investors

- Conduct thorough due diligence; never skip independent verification

With proper planning and professional guidance, Koh Samui property can be both a lifestyle upgrade and a sound financial investment. The island’s growing popularity, combined with Thailand’s relatively stable property market, offers opportunities that are increasingly difficult to find in comparable US coastal markets.

Ready to start your Koh Samui property journey? Contact Horizon Homes for personalised guidance through every step of the process, from property selection to closing and beyond. Our team understands the unique needs of US investors and can connect you with trusted legal and tax professionals to ensure your investment is both profitable and compliant.

*This guide is for informational purposes only and does not constitute legal or tax advice. Property laws and tax regulations change frequently. Always consult qualified Thai legal counsel and US tax professionals before making investment decisions.*

Frequently Asked Questions

Can I get a mortgage from a Thai bank as a US citizen?

Generally no. Thai banks rarely lend to foreigners. Some Singapore and Hong Kong banks offer financing for Thailand property, but expect 50%+ down payment and higher interest rates. Most US buyers purchase with cash or use home equity loans against US property.

Do I need to pay US taxes on rental income if I already pay Thai taxes?

Yes. The US taxes worldwide income for citizens. However, you can claim a Foreign Tax Credit for Thai taxes paid, which typically eliminates double taxation. You must still report the income on your US tax return.

What happens to my property if I die?

Without proper estate planning, your Thai property enters a complex probate process. For condos owned personally, heirs can inherit but must comply with foreign ownership restrictions. For leasehold structures, succession depends on lease terms. For company-owned property, company shares transfer according to shareholder agreements. A Thai will and proper structuring are essential.

Can I rent out my property on Airbnb?

Short-term rentals face increasing regulation in Thailand. Many condominium buildings prohibit short-term rentals entirely. Hotels and licensed properties have different rules. Check building regulations and local laws before counting on Airbnb income. Property management companies can advise on compliant rental strategies.

How do I repatriate rental income to the US?

Rental income can be transferred to your US account, but document everything for tax purposes. Your Thai bank will handle the currency conversion. Keep records of all transfers for both US and Thai tax reporting. Consider maintaining a THB reserve for property expenses to minimize transfer fees.

Is it better to buy in my personal name or through a company?

For most individual US investors buying a single condominium, personal name ownership is simpler and more tax-efficient. Company structures add complexity and US tax reporting requirements (Form 5471, potential Subpart F issues) that often outweigh benefits unless you have specific asset protection or estate planning needs. Consult both Thai and US tax advisors before choosing.

What is the Foreign Exchange Transaction Form (FET) and why does it matter?

The FET Form (formerly Thor Tor 3) is documentation from a Thai bank proving that funds for your condo purchase came from overseas in foreign currency. It’s required to register foreign ownership of a condominium. Without it, you cannot complete the ownership transfer. The funds must arrive in Thailand as foreign currency and be converted by the Thai bank, not sent as pre-converted THB.

How does the 49% foreign quota work?

Thai law limits foreign ownership in any condominium building to 49% of the total sellable floor area. Before purchasing, verify that the building hasn’t reached its foreign quota. Your lawyer should confirm this during due diligence. If the quota is full, you cannot register ownership even if you’ve already paid.

Can I buy land if my Thai spouse holds it?

While a Thai spouse can own land, structures where the foreigner effectively controls the land through the spouse face legal challenges. The Thai spouse must prove they purchased with their own funds, and the foreigner has no ownership claim. This structure has been successfully challenged in court. Leasehold or condominium ownership provides clearer legal standing.

What are the ongoing US reporting requirements after purchase?

Annual requirements include:

- FBAR (if foreign accounts exceed $10,000 aggregate)

- Form 8938 FATCA reporting (if foreign assets exceed thresholds)

- Schedule E for rental income (if applicable)

- Form 1116 for Foreign Tax Credit (if applicable)

These are ongoing obligations for the life of your ownership. Professional tax preparation typically costs $500-2,000 annually for international property owners.